General Liability for Contractors: Essential Protections for Minnesota Projects

One accident on a Minnesota job site can cost your contracting business hundreds of thousands of dollars. General liability for contractors isn’t optional. It’s the foundation that protects your assets when something goes wrong.

We at Maverick Risk Partners help contractors across Minnesota, Wisconsin, Iowa and the Dakotas understand what coverage they actually need and how to avoid costly gaps in protection.

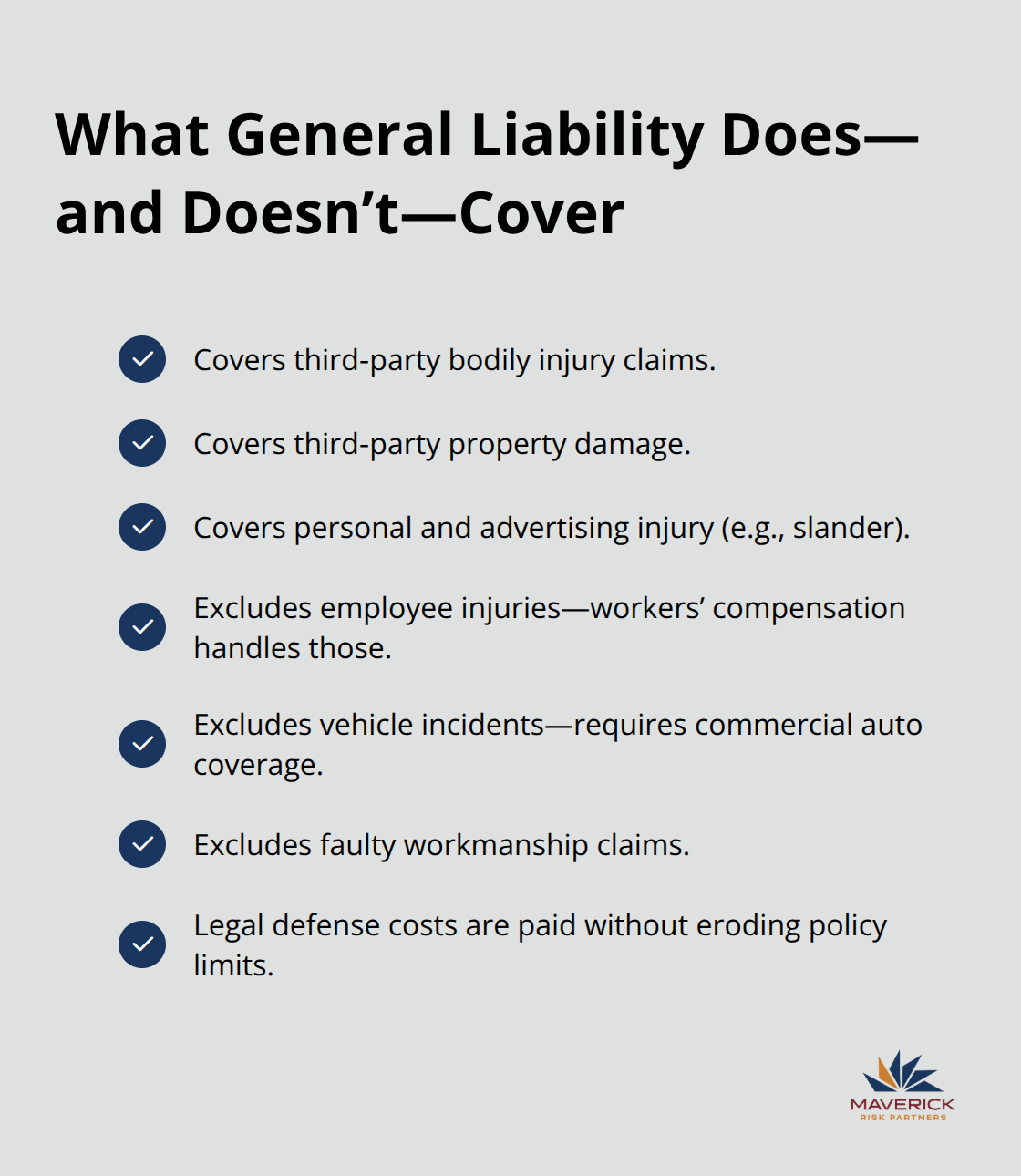

What General Liability Actually Covers

General liability insurance protects your contracting business when a third party claims you caused them bodily injury or damaged their property. General liability pays for medical expenses, lost wages, pain and suffering, settlements and judgements, and defense costs before and during court when you cause an injury or death to a third party. Some general liability policies can cover personal injury claims such as those for slander, libel or defamation. General liability also includes coverage for property damage which would include damage you cause to property owned by others. Standard policies do not cover employee injuries (workers’ compensation handles that), auto-related incidents (commercial auto does that), or faulty workmanship claims (the dreaded “Your Work Exclusion”). Many contractors mistakenly believe general liability covers everything on a job site but it doesn’t.

Why Coverage Limits Matter More Than State or Contract Minimums

Average construction claims regularly exceed $500,000, which means relying on minimums leaves you personally liable for the gap. Most Minnesota contractors should carry at least $1 million per occurrence, with a general aggregate limit of at least $2 million. For municipal or government projects, larger projects, road work, or high-risk projects, even higher limits are strongly recommended. Most contracts will clearly state the minimum the contract holder requires, but the disclaimer states that the contractor is required to carry limits high enough to meet their financial obligations. This means that even if the contract only requires a $1 million limit, the contractor should carry or the job exposure makes it a candidate for higher limits.

How Legal Defense Costs Can Be Paid By Your Insurer

Legal defense costs are usually paid separately from your policy limits as long as your general liability is written on an occurrence form. Be careful of general liability policy forms that are written on a claims-made basis or that have a specific maximum for legal defense. You might find yourself without enough defense coverage for the entire claim process. When the defense coverage is “outside” your policy limits, the insurer covers court expenses, attorney fees, expert witness expenses, etc. without reducing your total available coverage. When the defense coverage is “inside your policy limits,” all of the costs of defending the claim will reduce your total available limit of liability.

A word of caution – your insurer is only required to provide your defense and cover defense costs until they’ve paid out the policy limit you purchased. If you purchase a $500,000 general liability limit policy and have a claim estimated at $650,000, your insurer can pay the other party the “policy limit” (in this case that is $500,000) stop defending you. If the insurer determines that the cost of the damages of the claim will be close to or exceed the limit you purchased, your insurer can pay the full amount of coverage you bought and no longer has to pay for your defense. This does not stop the other party from continuing to sue you, but it does make you personally responsible for defense costs after that. This is why we strongly recommend that contractors carry an umbrella or an excess liability policy so they will always have enough coverage to keep the insurance company in the position of defense.

Structuring Your Policy for Contract Requirements

Your coverage documents should name your business as the “named insured” on the policy. If you have written agreements with contract holders that specifically ask for special language, you can extend your policy coverage to those contract holders. Contract holders might ask for their entity to be listed as an “additional insured” and may ask to have additional special language such as primary and non-contributory, and waiver of subrogation. Most of these endorsements require that the agreement to add the special language must be in writing with the contract holder before the loss to be valid and cannot be added based on verbal agreements or after a loss. These endorsements protect your clients and aligns with what most project owners (and the insurers of project owners) expect and require before work begins. Understanding these requirements upfront prevents delays, unexpected costs and expenses and coverage disputes later.

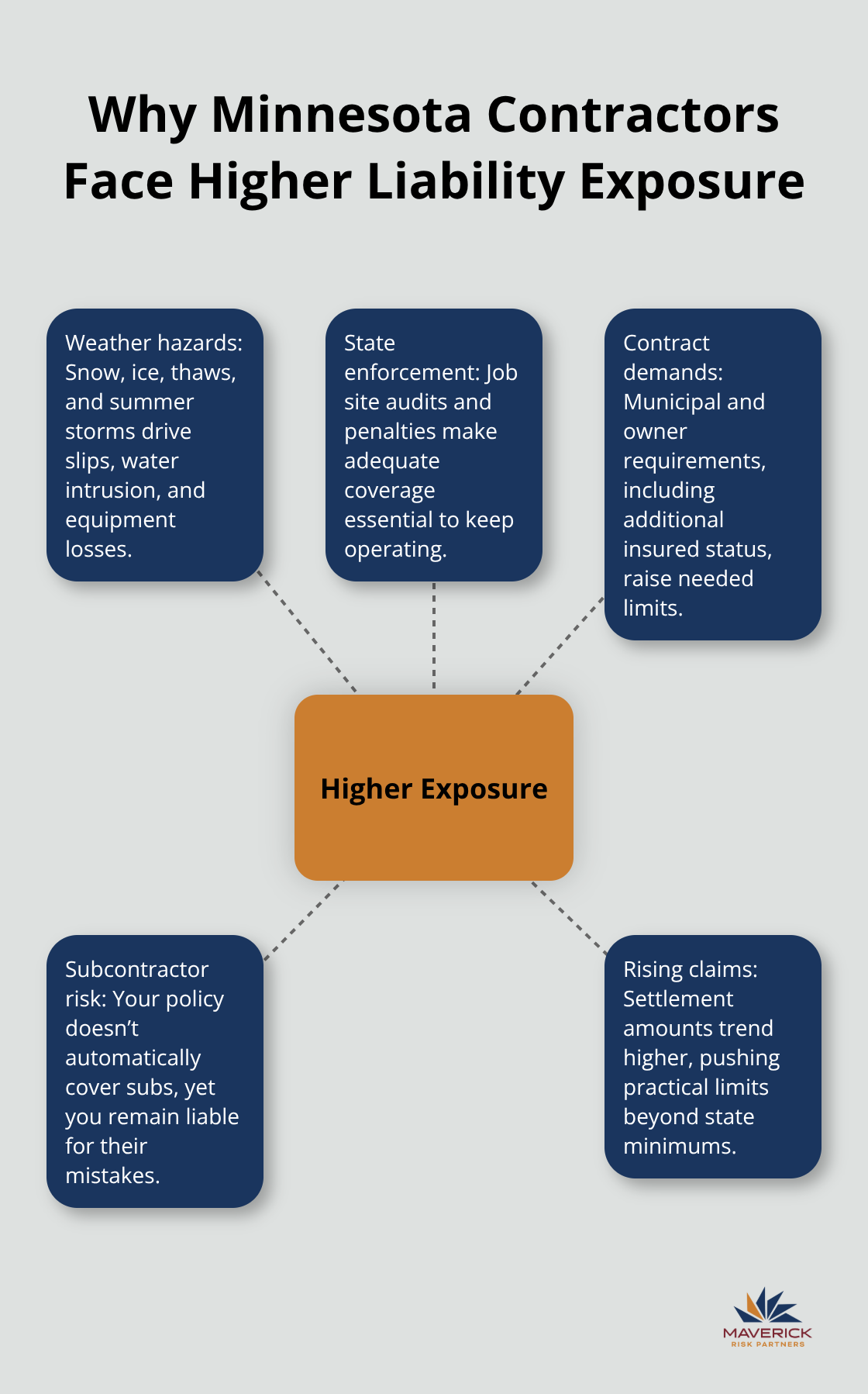

Why Minnesota Contractors Face Higher Liability Exposure

Weather and Climate Create Year-Round Job Site Hazards

Minnesota’s climate generates job site hazards that directly increase your liability risk throughout the year. Winter weather causes slip-and-fall injuries on icy surfaces and roofs, while spring thaws damage adjacent properties through water intrusion and foundation issues. Summer storms bring equipment damage and worker exposure claims. These seasonal patterns mean your liability exposure shifts constantly, requiring coverage limits that account for the full range of Minnesota weather conditions.

State Enforcement and Regulatory Requirements

The Minnesota Department of Labor and Industry conducts regular job site audits, and contractors found with inadequate coverage face license suspensions and fines. This enforcement reality means your coverage limits directly impact your ability to operate legally. Municipal projects add another layer of complexity because clients require you to name them as additional insured on your policy and may have other special language to meet regulatory compliance. If your policy limits fall short of what clients contractually require, you won’t win bids or you’ll face work stoppages mid-project while coverage disputes get resolved.

Subcontractor Exposure and Coverage Gaps

Subcontractor exposure is where most Minnesota contractors discover their coverage gaps too late. Mistakes in managing subcontractor exposures can cause significant compliance issues, unexpected premiums at audit, uncovered claims and damaged relationships with contract holders. Your general liability policy does not automatically extend to the work performed by subcontractors you hire. Meaning if a subcontractor causes property damage or injures someone on your job, you remain liable even though you didn’t perform the work. And if your insurance coverage is not done correctly, you might be liable and also uninsured. Requiring subcontractors to provide certificates of insurance protects you, but only if you have a fully executed, valid subcontractor agreement, their coverage actually exists, it has the right endorsements and meets your project requirements. Many contractors skip these steps to save time on small jobs, then face six-figure claims when a subcontractor’s negligence damages a client’s building.

No Coverage for Your Faulty Workmanship

Most general liability policies use a standard ISO form referred to as CG 0001. Carriers use this form or their own version for general liability that is on an occurrence basis. The most commonly used form right now is CG 00 01 04 13 (which means it is form CG0001 edition date 04/13). On page 5 of 16 of this policy form shows policy exclusions. Exclusion “I” is titled “Damage To Your Work” and reads that this policy does not provide coverage for property damage to “your work” Arising out of your work or any part of your work. This means if you do bad work or your work fails, this policy will not provide coverage for your poor work or faulty workmanship. Many contractors do not understand this standard exclusion in general liability policies. There are times you can purchase an endorsement to provide some limited coverage for certain situations involving your work but that requires an endorsement.

Exclusion “I” titled “Damage To Your Work” continues by stating that the exclusion does not apply if the damaged work or the work out of which the damage arises was performed on your behalf by a subcontractor. Yeah, right?? Historically, this has been how a general contractor or the contract holder was protected when the damage was caused by a subcontractor. But most contractors were not aware that carriers have been including another form in their policies that completely removes that second paragraph for work by subcontractors. This new exclusion is a Total Subcontractor Exclusion and the most common form is CG 22 91. The form was originally created in 2001 (yes, 24 years ago) and uses a 10/01 version date. The form wasn’t used frequently by carriers back in 2001, but in the last five years it is being added to the majority of standard contractor policies. Many times without the insured being aware because you have to read the policy to see the added exclusion. Some carriers will allow you to remove the exclusion as long as you provide proof of complying with their subcontractor agreement and minimum coverage requirements. The exposure of subcontractors is very complex and requires attention and involvement between the contractor and the insurance agent.

Rising Claims and the Cost of Inadequate Limits

Construction claims in Minnesota have grown consistently, with average settlement amounts regularly reaching significant levels for bodily injury or structural damage cases. Contractors carrying only minimum coverage are personally responsible for everything above that threshold. A substantial claim can leave you liable for amounts that exceed your policy limits, including costs of defending your case, which can impact a small to mid-sized contracting business. Most Minnesota contractors should carry adequate per occurrence limits with appropriate general aggregate limits, and for road work or large commercial projects, higher limits become the practical baseline. These limits protect your business when claims exceed what your current policy covers, and they align with what project owners expect to see before awarding contracts.

Choosing the Right Coverage Limits for Your Project

Match Coverage Limits to Project Size and Scope

Start with your project size and scope, not with contract or carrier minimums. A small residential repair job can support different coverage than a $2 million commercial project or municipal work or road work. For most contractors, you should carry at least $1 million per occurrence with a $2 million aggregate minimum. Large, commercial, municipal and government projects typically exceed these minimums because actual claims often run higher. Road construction, utility work, and projects involving excavation or heavy equipment demand $2 million per occurrence limits or more because injury and property damage claims in these trades regularly exceed $1 million.

Calculate Your Premium Against Your Risk Exposure

The practical approach is to review your contract requirements first. Most clients specify minimum limits in their RFP or bid documents. You would need to at least meet those contract limits to work with those contract holders. Then you should assess how much business your company does and the potential value of the properties you’re working in. You can never really properly estimate liability limits to protect for all of the potential bodily injury claims. But you can look at the properties you’re doing your work in for some ideas on minimum limits. For work in residential homes valued at under $600,000, a policy limit of $1,000,000 for an occurrence might suffice. Homes valued at over $1,000,000 or smaller commercial buildings warrant limits between $2,000,000 and $5,000,000. If you’re working in larger commercial buildings where the value of the building is $20M, $50M or $100M, then limits above $5,000,000 might be warranted.

Ask yourself – if you’re doing work inside a client’s building and you accidentally start a fire that causes significant damage throughout the building, how much coverage is enough coverage for the buildings you’re working in?

General liability premiums in Minnesota for small, low-risk, single-owner artisan contractors might range from $500 – $800 annually. These contractors likely have no subcontractors or very little subcontractor exposure. They have little to no tools, and they have little to no materials or equipment. Premiums for contractors with higher percentages of subcontractor use, higher-risk type of work, work that involves heights, and larger projects might expect to pay $2,500 – $5,000 on the low end to thousands of dollars on the high end.

Identify Critical Policy Exclusions

Policy exclusions are where coverage actually fails. Standard general liability excludes employee injuries (workers’ compensation covers that), vehicle-related damage (commercial auto handles that), and faulty workmanship claims entirely. These gaps mean you need additional policies or endorsements to cover your complete exposure. If you use vehicles for business, your personal auto policy likely excludes business use, leaving you uninsured during job site travel and commercial auto insurance is then non-negotiable. For projects involving environmental work, pollution claims are excluded from standard general liability, so environmental liability insurance becomes essential.

Add Endorsements That Match Your Contracts

Endorsements add specific protections: additional insured status protects your clients for claims where you are negligent but they are the contract holder, contractual liability extends coverage to hold harmless agreements you sign with clients, and products liability protects you if materials or equipment you supplied cause injury. Many Minnesota contractors require subcontractors to carry additional insured endorsements naming the general contractor, but you must verify these endorsements actually exist by requesting the certificate of insurance and copies of the endorsements before work begins.

Work with an Agent to Close Coverage Gaps

An independent insurance agent familiar with construction risks can identify which endorsements your specific trades need and which gaps require separate policies. Agents who work with multiple carriers can often reduce premiums by 15-25 percent and sometimes even 50% percent compared to going directly to a single insurer, and they have access to specialty markets for high-risk contractors that standard carriers won’t quote.

An independent agent can align coverage limits and endorsements with your actual project risks and contractual requirements, preventing the gaps that create costly disputes after claims occur.

Final Thoughts

General liability for contractors protects your business when you are involved in a claim of property damage or bodily injury that leaves you exposed to six-figure gaps. Many Minnesota contractors operate safely with $1 million per occurrence and $2 million general aggregate and many also have a $1, million umbrella excess liability policy too. Your policy limits, endorsements, and exclusions must align with your actual project risks and contractual requirements before you bid work.

Requiring subcontractors to carry additional insured, waiver of subrogation, primary and non-contributary endorsements, naming your company as an additional insured on their policy, and understanding what your coverage excludes prevent costly surprises after claims occur. An independent insurance agent can identify which endorsements your specific trades need and which gaps require separate policies like commercial auto, workers’ compensation, or environmental liability. A thorough exposure and coverage review can often reduce your total premium by 15 to 25 percent compared to shopping with a single carrier. These operational steps transform general liability from a checkbox item into a strategic protection that actually covers your exposure.

We at Maverick Risk Partners work with contractors in Minnesota, Wisconsin, Iowa and the Dakotas to build coverage that protects your business rather than just meets minimums. Contact us to review your current coverage and identify the gaps that could cost you thousands.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional in our office for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.