Minnesota Department of Labor and Industry

, Running a contracting business in Minnesota means understanding your workers compensation obligations. State law requires specific coverage requirements, and getting this wrong can result in serious penalties.

We at Maverick Risk Partners help contractors navigate contractor workers compensation Minnesota requirements so you can focus on your work. This guide walks you through what’s legally required, what coverage types matter most, and how to find the right policy for your operation.

Legal Requirements for Contractor Workers Compensation in Minnesota

What Minnesota Law Actually Requires

Minnesota law mandates that contractors carry workers compensation insurance for all employees, with no exceptions based on company size. Even if you only have a part-time office employee or estimator, you’re required to carry workers’ compensation in Minnesota. The Minnesota Department of Labor and Industry enforces this requirement strictly, and the consequences for ignoring it are severe. The construction industry also has additional rules related to workers’ compensation requirements when subcontractors are used in addition to or in replacement of employees. The line between employee and subcontractor is one that every contractor should know well.

As of March 1, 2025, independent contractor status in the construction field is determined by a 14-factor test, but if a worker doesn’t meet ALL of the criteria, they’re classified as an employee and must be covered. This distinction matters enormously because misclassifying someone as an independent contractor when they’re actually an employee exposes you to significant liability.

The state doesn’t set a single coverage minimum dollar amount that applies universally. Instead, your policy must cover medical expenses, wage loss benefits, and and other policy terms and limits (such as employers liability) available in the market or defined by statute. What this means practically is that you need a policy that handles medical care for injured workers, replaces a portion of their wages during recovery, and protects your business if an employee sues.

The Real Cost of Non-Compliance

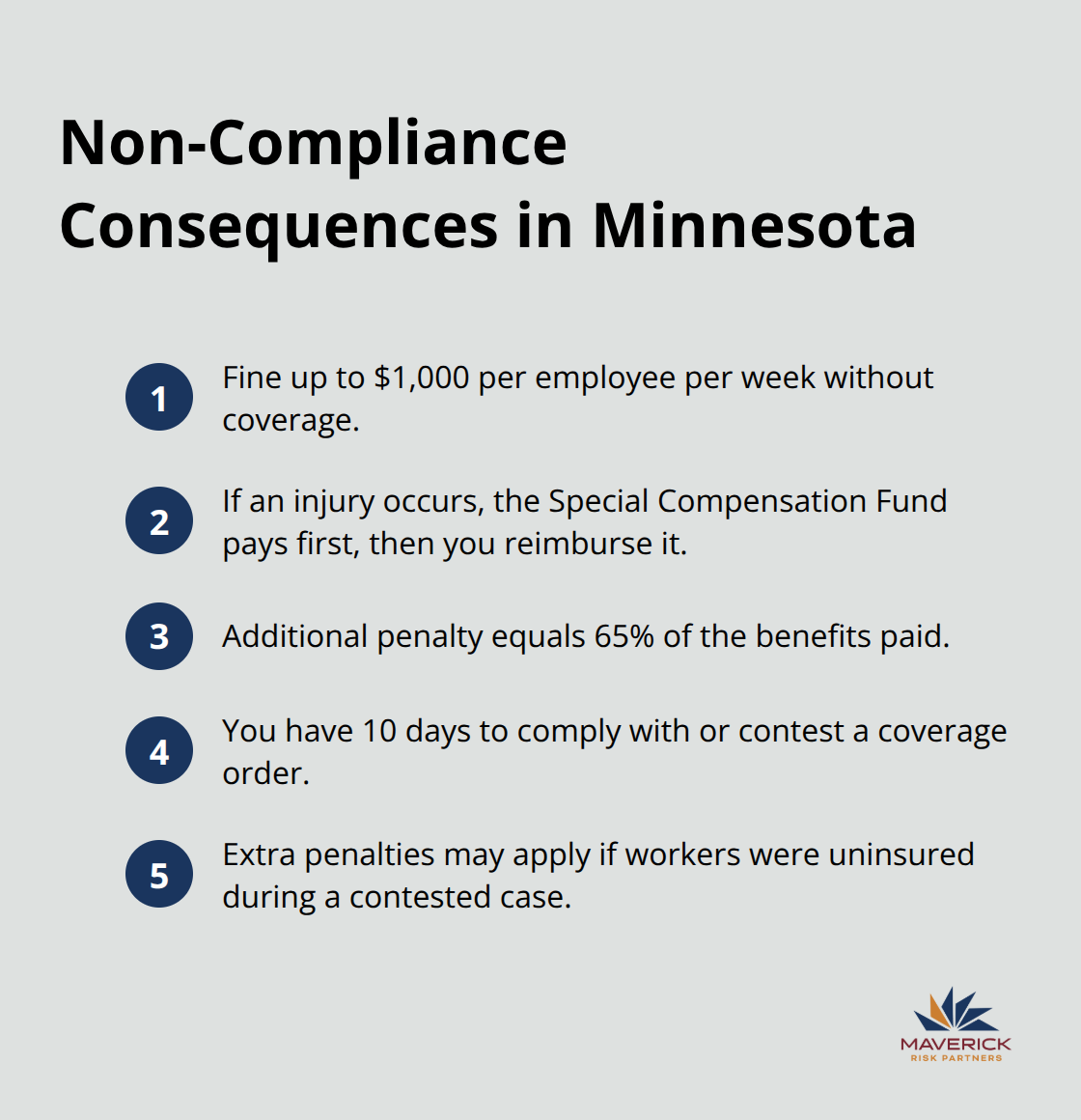

Penalties for non-compliance are not theoretical warnings. If you operate without coverage, Minnesota law allows fines up to $1,000 per employee per week for each week they remain uninsured. There does not need to be any injuries for the penalty to be assessed! The penalty applies if you have employees or subs that fail to meet the 14 point test and it is found out or someone reports you. If an injury occurs and you have no policy, the Special Compensation Fund pays the injured worker’s benefits, but then you must reimburse that fund plus an additional penalty equal to 65 percent of the benefits paid. This creates a compounding financial disaster that most contractors cannot absorb.

The Minnesota Department of Labor and Industry gives employers 10 days to comply with a coverage order or contest it. That means you have 10 days to get new coverage or prove you had it. If you don’t respond within that window, the order becomes final and cannot be appealed. If you do contest and lose, a workers compensation judge can impose additional penalties if uninsured workers were employed while the case was pending.

Finding Coverage When Standard Carriers Decline You

The assigned risk pool exists specifically for contractors who cannot obtain coverage in the regular market, so claiming you can’t find a policy is not a viable defense. This pathway ensures that even high-risk operations can secure the coverage Minnesota law requires. Always work with an experienced commercial insurance broker when navigating workers’ compensation for your contracting business. Policies are available even if you have no payroll and/or only have subcontractors, yet are contractually required to carry the coverage.

Understanding these requirements and acting on them immediately protects your business from financial ruin. The next section covers the specific types of coverage your policy must include and what additional protections you should consider for your operation.

Types of Coverage and What Contractors Need

Medical Benefits Cover All Work-Related Treatment

Your workers compensation policy in Minnesota must cover medical expenses for any injury that arises from work. Your policy pays for all reasonable medical treatment related to a work injury, including doctor visits, surgeries, physical therapy, and prescription medications. Minnesota law places no dollar cap on medical benefits, so even expensive treatments receive coverage if they are medically necessary. This unlimited medical protection means you won’t face surprise bills for legitimate injury care, and injured workers receive the treatment they actually need rather than what fits a budget.

Wage Loss Protection Replaces Worker Income

When an injured worker cannot work, your policy must replace a portion of their income. Temporary total disability pays roughly 66.67 percent of the worker’s average weekly wage while they remain completely unable to work. The state adjusts maximum weekly benefit amounts annually. For the 2025-2026 benefit filing, the maximum weekly benefit was approximately $1,536.84 for dates of injury on and after October 1, 2025. This means a contractor earning $2,000 per week would receive about $1,334 during total disability. Injured workers expect income replacement, and your policy must deliver it consistently. Without adequate wage loss coverage, workers face financial hardship and may pressure you to return them to work before they’re medically ready, creating liability for you.

Employer Liability Coverage Protects Your Business

Minnesota allows employees to sue employers for workplace injuries in certain situations, and employer liability coverage defends you against these lawsuits. While Minnesota statutes state that workers’ compensation insurance is the exclusive remedy for employee injuries, there are some exclusions to this rule only employer’s liability coverage can respond to. Two examples of lawsuits from employee injuries include 1) Loss of Consortium from the injured worker’s spouse or family, or 2) consequential bodily injury where a family member alleges they had an injury (heart attack, stroke) because of the employee’s injury. Another example involves “Third Party Action Over” claims. This is where your injured employee sues a third party (like the owner of the project or the general contractor) alleging their conduct contributed to the employee’s injury. Basically, the injured employee is not satisfied with the workers’ compensation, so they “go over” their employer to sue a 3rd party. In this situation, the injured worker collects workers’ compensation from you and sues the third party.

Contractual Liability in your Contractor Agreements

Many times there is contractual liability in construction agreements that specifically passes this liability back to the employer (you). The indemnification clauses in construction agreements are often very strong. Many contractors don’t read these agreements and do not have them looked at by a lawyer before signing. It’s the contractual liability in the contract that makes these “Action Over” claims important to cover with proper Employer’s Liability limits.

Employer’s Liability coverage pays defense costs, legal fees, settlements or judgments up to your policy limits when an employee or their spouse or family successfully sues your business. When you look at a Minnesota workers’ compensation insurance policy, the limits shown on that declarations page are for employer liability coverage. That workers’ compensation for medical expenses does not have a maximum limit or cap. The Employer’s Liability is what is represented by the limits on your policy. Without adequate employer liability limits, a serious injury lawsuit can exceed your coverage and hit your personal assets. Contractors working on larger projects or employing multiple workers should carry $500,000 to $1,000,000 in employer liability rather than the state minimum available limit of $100,000 per accident. The cost to carry higher limits of $500,000 or $1,000,000 is very, very low.

Optional Coverage Addresses Specific Contractor Risks

Beyond required components, optional coverage deserves serious consideration depending on your operation’s specific risks. Equipment coverage protects tools and machinery on job sites, addressing a real risk contractors face. Pollution liability applies if your work involves hazardous materials, and cyber liability protects your business if you handle employee data. The assigned risk pool available through the Minnesota Workers Compensation Insurers Association covers contractors that standard carriers reject, but assigned risk policies can cost significantly more so maintaining a clean safety record and proper worker classification saves substantial money over time. If you had to start in the assigned risk pool, make sure to contact an experienced commercial insurance broker to move you out of the assigned risk pool as soon as possible.

Selecting the right coverage level requires honest assessment of your specific business risks and operations. The next section walks you through how to evaluate carrier options and work with an agent to build a policy that actually protects your contracting business.

How to Choose the Right Workers Compensation Policy

Gather Accurate Payroll and Job Classification Data

Start by collecting your payroll records and job classifications for the past one to two years. Carriers need accurate information about how many workers you employ, what types of work they perform, and your total annual payroll to quote you fairly. If you misrepresent this data to obtain a lower premium, you will be charged back the difference during the audit period and the carrier choose to cancel or non-renew your policy if they feel there was intentional misrepresentation.

Understanding Workers Compensation Audits

All workers’ compensation policies are audited unless the carrier audits monthly through payroll reporting. This means that you will only pay for premium for your actual payroll. If you overestimate your payroll, you will get a credit. You underestimate your payroll; you will get a bill. You must complete an audit for each policy term. If you don’t complete an audit, the carrier reserves the right to charge additional costs, fees, and penalties for non-compliance. Sometimes this can be as much as 200% of your original premium. And non-compliant audits prevent you from getting coverage from any carrier that you have a non-compliant audit open with, including the Minnesota State Assigned Risk Pool.

Job Classification Data – Workers Misclassification

Minnesota has some very strict, and expensive, worker misclassification rules and penalties. Employers can face penalties of up to $10,000 for each employee that it fails to classify or treat as an employee pursuant to Minnesota statutes sections 181.722 or 181.723. The construction industry is very specific and strict. Minnesota Statutes section 181.723, subd. 3, states “an individual who provides or performs building construction or improvement services for a person that are in the course of the person’s trade, business, profession or occupation is an employee of that person and that person is an employer of the individual.” This means that all contractors and subcontractors are considered employees unless they meet the independent contractor test. In other words, if you are hiring an individual to provide or perform services that are in the course of your trade, business, profession or occupation, the individual is your employee unless all the elements outlined in Minnesota Statutes section 181.723, subd. 4, are satisfied (The 14-Factor Test). Contractors frequently understate payroll or misclassify workers to reduce costs, but this strategy backfires when claims occur and the insurer or state investigates.

Verify Contractor Licensing

Check the Minnesota Department of Labor and Industry Contractor License Lookup Directory to verify that any contractor you consider holds proper licensing in Minnesota. Some trades, such as electrical, plumbing, mechanical, remodelers and builders, require specific and separate licensing. Some licensing requires annual continuing education keep the license. Minnesota also requires Minnesota Contractor Registration if other specific licensing is not required.

An experienced commercial agent familiar with Minnesota construction can often review multiple carriers and help you compare not just price but coverage terms, deductible options, audit processes and claims-handling reputation. When evaluating quotes, avoid fixating solely on premium cost. Especially because premium is audited and is tied to the rate per $100 of payroll. There can be a quote that looks lower on the surface, but inaccuracies in the quote would result in a higher premium at audit. Using the wrong class codes, inaccuracies in estimated payrolls, errors in factoring the inclusion and exclusion rules for owners and partners, and missing possible program credits, can result in wildly different quotes.

Match Coverage Limits to Your Specific Operation

Your business risks depend on your specific operation, so a roofing contractor’s needs differ from a specialty trade contractor’s. Assess whether you work at heights, handle hazardous materials, operate heavy equipment, or work on large commercial projects versus residential jobs. Each risk profile justifies coverage limit evaluation. A specialty trade contractor working solely on minor residential renovations might carry $500,000 or $1,000,000 in employer liability. While a contractor bidding commercial projects should carry $1,000,000 and make sure to include their employer’s liability coverage under their umbrella/excess liability policy. General contractors on large projects often require subcontractors to carry minimum liability limits of $1,000,000 and may require an umbrella or excess liability policy.

Consider a Specialty Policy that Provides Training and OSHA assistance

All workers’ compensation policies are not created equal. Most workers’ compensation policies are considered “Guaranteed Cost” policies. This means there’s an agreed-upon rate for the coverage, and you pay it regardless of how good you run your business and how well you manage losses. But there are carriers that specialize in contractor workers’ compensation policies that provide more and only provide workers compensation and only serve the construction industry. Some construction specialty carriers provide workers’ compensation coverage on a reporting basis so that your premiums match your incomes. They have specialty claims departments that are exceptionally trained to handle construction-related injuries. Specialty carriers can offer training, support, OSHA assistance and more. Choosing a carrier partner that helps keeping your workers’ compensation claims managed results in lower premiums to you.

Consider a Specialty Policy that Pays You Dividends

There are also specialty carriers that will pay you back dividends when you have lower losses than projected and/or when the group has overall lower losses than projected. These policies are often referred to as “dividend” or “loss-sensitive” plans. A workers’ compensation dividend plan is a policy type used where insured employers can share with the insurance company in the profitability of their account. Simply put, these dividend plans reward employers for having fewer claims. It’s still a workers’ compensation policy, but just with a benefit available to you. There are different varieties of these “dividend” or “loss-sensitive” plans it’s important to understand what type of plan you would best benefit from. These plans are only a good fit for employers who do invest in safety and loss control and want to continue to do so. But the rewards can be significant. If you’re a Minnesota contractor with payroll in the construction field and you are not on a “dividend” or “loss-sensitive” plan but want to learn more, contact us to see what might be available to you.

Work with an Agent Who Understands Construction

Your agent should ask detailed questions about your operations, not simply hand you a standard quote. The best agents in Minnesota understand construction, know which carriers specialize in contractor business, and can explain why they recommend specific coverage limits for your situation rather than offering the cheapest option available. An agent who takes time to understand your operation helps you avoid coverage gaps that surface only when you need the protection most.

Final Thoughts

Minnesota workers compensation requirements for contractors are not optional guidelines you can negotiate around. State law mandates coverage for all employees, penalties for non-compliance reach $1,000 per employee per week, and misclassification exposes you to reimbursement obligations plus 65 percent penalties when injuries occur. The 14-factor test for independent contractor status in building construction means many subcontractors you hire could easily qualify as employees requiring coverage, not contractors exempt from your policy.

Your contractor workers compensation Minnesota policy must cover medical benefits, wage loss protection, and employer liability to defend against employee lawsuits. Selecting the right policy requires accurate payroll data, accurate classification, and coverage limits matched to your actual business risks rather than the lowest premium available. The assigned risk pool exists as a safety net if standard carriers decline you, but assigned risk premiums often run substantially higher (some are 40 to 60 percent higher) than standard market rates, making proper worker classification and a clean safety record financially valuable. Specialty carriers that provide training and support and even dividends are available as an option to contractors for their workers’ compensation insurance

We at Maverick Risk Partners help Minnesota contractors secure coverage that protects your business and employees. Contact us to discuss your coverage needs and connect with carriers that understand your operation.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional in our office for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.