IBM's 2024 Data Breach Report

A data breach can cost Minnesota businesses an average of $4.88 million, according to IBM’s 2024 Data Breach Report. Cyber attacks are hitting companies harder and more frequently than ever before.

Cyber liability coverage in Minnesota protects your business from these financial disasters. We at Maverick Risk Partners help companies understand what this coverage actually covers and why it matters for your bottom line.

Why Minnesota Businesses Face Real Cyber Risk

The Accelerating Threat Landscape

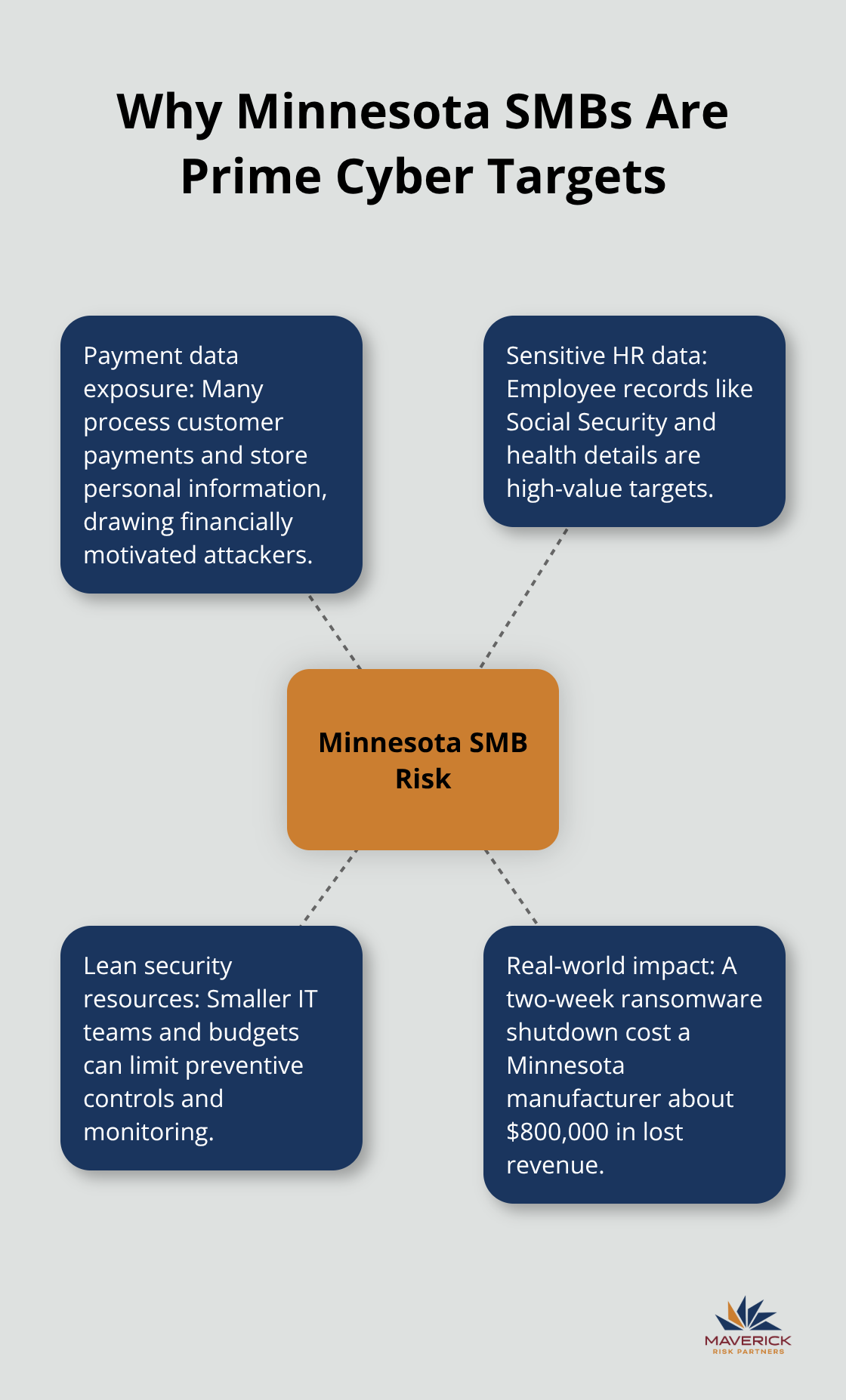

Cyber attacks in Minnesota are accelerating. Small and mid-sized businesses across the state have become prime targets because they process customer payments and hold sensitive employee data while often running leaner IT security operations than larger corporations. A manufacturing company in Minnesota experienced a ransomware attack that shut down production for two weeks, costing the business approximately $800,000 in lost revenue alone before factoring in recovery expenses. That’s the reality facing businesses that lack adequate cyber protection.

The True Financial Cost of a Breach

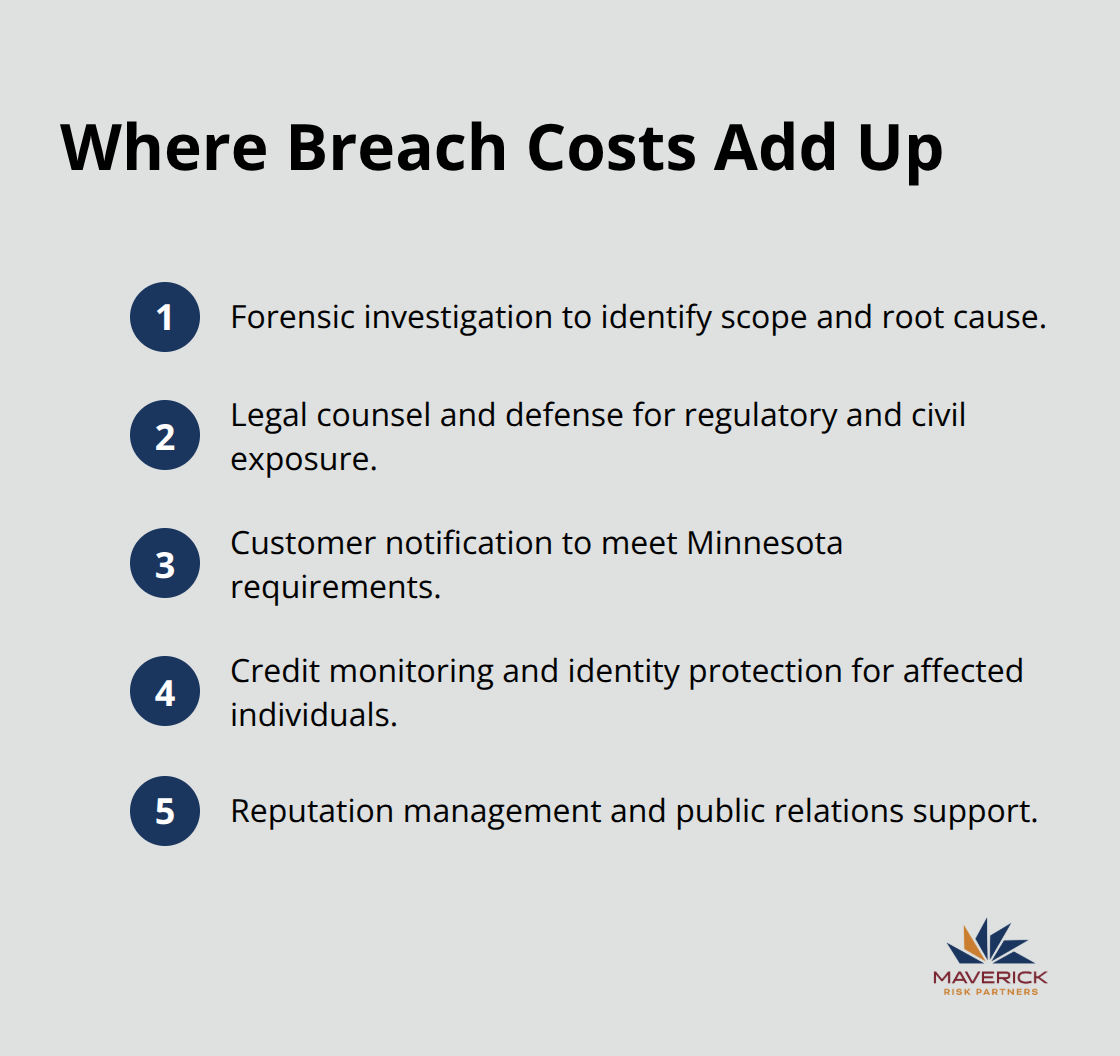

The financial toll extends far beyond downtime. IBM’s 2024 Data Breach Report shows that the average global breach cost has reached USD 4.88 million when accounting for forensic investigation, legal fees, notification expenses, credit monitoring services, and reputational damage. One St. Paul city cyberattack cost the municipality $2.5 million in unplanned response expenses including overtime pay and new equipment purchases, with over $2 million directed toward external consulting and specialized cybersecurity support. The total cost to the city was over $2.5 million and while there was an undisclosed ransom demand, the city did not pay the ransom demand. These aren’t theoretical numbers-they represent real operational disruptions and financial strain that threaten business continuity.

Compliance Obligations You Cannot Ignore

Minnesota state law requires immediate action when a cybersecurity event occurs. Under Minn. Stat. § 60A.9853, you must notify the Commissioner of Commerce no later than five business days from determining that a cybersecurity incident happened. This notification requirement applies to all Minnesota licensees regardless of business size. Failure to comply creates additional legal and financial exposure beyond the breach itself.

When you have clients that reside in or purchase your goods or services from other states, you’re required to comply with the cyber security laws of the state that your client resides in. as of March 2026, over 20 states have enacted very comprehensive data privacy laws (including Minnesota, California, Texas, Colorado, etc.). All 50 states have breach notification laws requiring you to notify individuals if their personal data is compromised. It is very important to know the consumer privacy laws in the states your customers are in.

The state mandates that affected individuals receive notification of any compromise involving their personal information, and these notification costs add up quickly when you contact hundreds or thousands of customers. Cyber liability coverage handles these mandatory notifications and the associated legal compliance expenses, protecting your business from penalties and enforcement action while you focus on recovery and reputation management. Understanding what your current coverage actually protects-and what gaps exist-becomes your next critical step.

What Your Cyber Liability Coverage Actually Protects

Immediate Breach Response Costs

Cyber liability coverage handles the financial fallout from a breach that general business policies simply ignore. When a breach occurs, your business faces immediate costs that multiply quickly: forensic investigators determine what happened, lawyers assess your legal exposure, notification services contact affected customers, credit monitoring protects victims, and public relations specialists manage your reputation. A single breach involving 5,000 customer records can trigger $50,000 to $150,000 in notification and forensic costs alone before any legal action materializes. Cyber liability coverage absorbs these first-response expenses, which means your business avoids a cash crisis while recovering.

The policy covers the forensic investigation to determine the breach’s nature and extent, legal reviews to understand your liability exposure, notification costs required by Minnesota law, credit monitoring and identity theft protection for affected individuals, and public relations support to manage media response. Without this coverage, you write checks from operational funds while your business is already disrupted.

Business Interruption and Recovery Expenses

Cyber liability coverage protects against business interruption losses and third-party liability claims. If a ransomware attack shuts down your systems, the policy covers lost income during downtime and extra expenses to restore operations faster, such as emergency IT contractors or temporary equipment rentals. The St. Paul city attack illustrates this reality: over $2 million of the $2.5 million response cost went to external consulting and specialized cybersecurity support that accelerated recovery. The policy also covers your legal defense if customers or partners sue over the breach, including settlement costs if litigation becomes necessary.

Additionally, cyber liability covers legal fees and expenses to defend against regulatory investigations, which Minnesota requires within five business days of a breach. These recovery expenses accumulate rapidly when you contract external specialists to restore systems and validate data integrity.

What General Liability Policies Miss

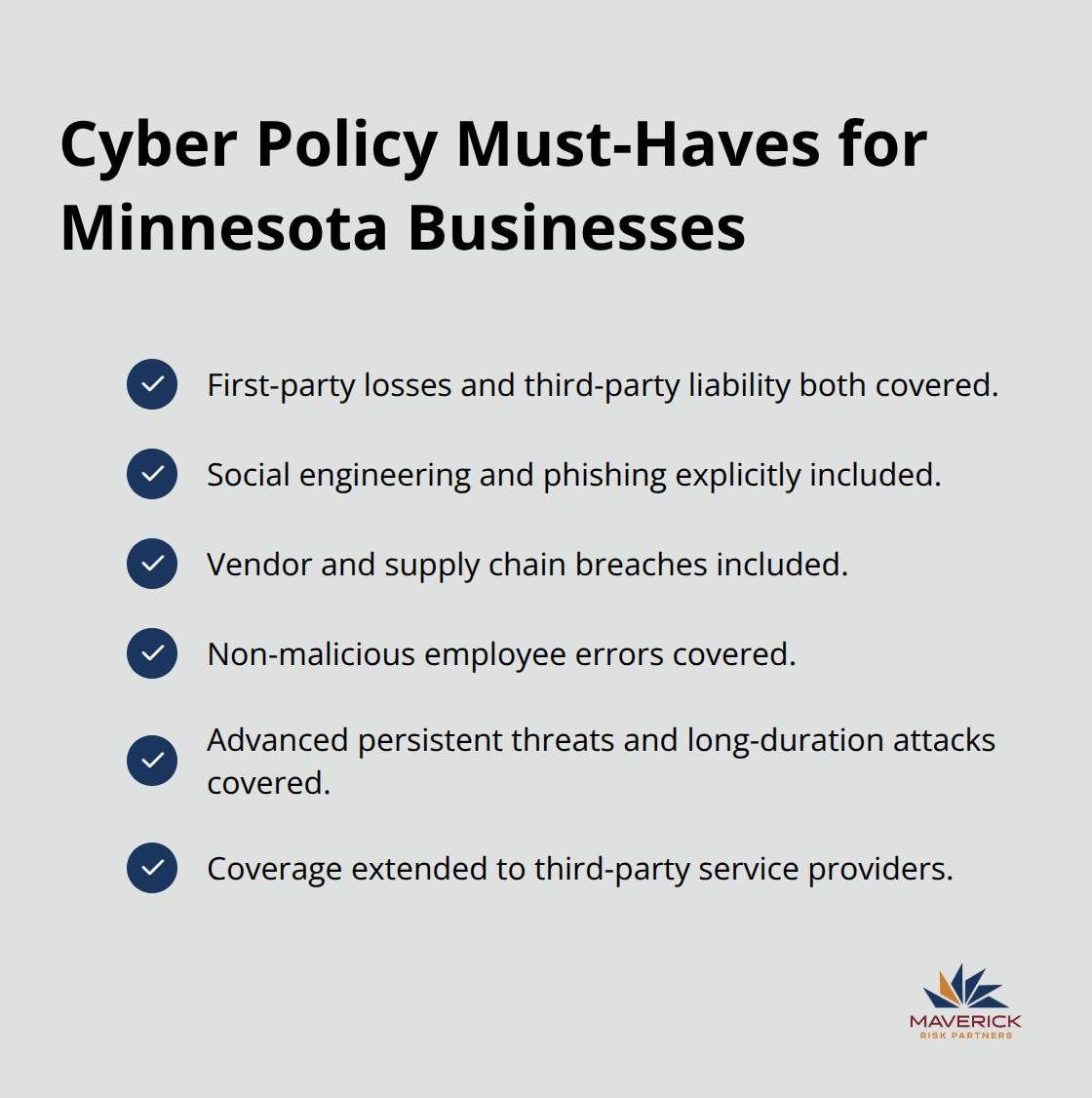

Many Minnesota businesses mistakenly assume their general liability or management liability policies cover cyber incidents-they don’t. General liability focuses on bodily injury and property damage from your products or operations, leaving cyber losses completely unprotected. Stand-alone cyber policies are substantially more comprehensive than cyber coverage bolted onto existing policies because they’re designed specifically for digital threats.

When evaluating coverage, verify that your policy covers both first-party losses (your own recovery costs) and third-party losses (customer lawsuits), and confirm the policy includes social engineering attacks such as phishing since these represent a major attack vector for Minnesota businesses. The specific terms, limits, and exclusions vary significantly across carriers, so comparing policies side-by-side reveals which protection actually matches your operational risks.

Identifying Your Coverage Gaps

Your current policy may leave dangerous gaps unaddressed. Confirm whether your coverage extends to third-party service providers and whether your vendors maintain their own cyber insurance, since supply chain vulnerabilities expose your business to indirect breach liability. Verify the policy handles non-malicious employee actions that compromise data, as these incidents occur more frequently than many business owners realize. Check whether the policy covers advanced persistent threats (APTs) and long-term cyber campaigns, since these attacks can span months or years and require extended coverage windows.

The specific attack types your policy covers-targeted attacks only, or all types-matter significantly when threats evolve. Understanding these distinctions now prevents costly coverage disputes after an incident occurs, and this clarity becomes essential as you evaluate whether your current protection actually matches the threats Minnesota businesses face today.

Common Cyber Threats Targeting Minnesota Companies

Ransomware Attacks That Halt Operations

Ransomware has become the dominant threat Minnesota businesses face today. Attackers encrypt your systems and demand payment to restore access, forcing you into an impossible choice: pay the ransom or lose weeks of operations while IT specialists work to decrypt files. The Cybersecurity and Infrastructure Security Agency reports that ransomware attacks have accelerated across the Midwest, with manufacturing, healthcare, and local government entities hit hardest. A Minnesota manufacturing company that experienced a two-week production shutdown lost $800,000 in revenue before accounting for system recovery costs. Your cyber liability coverage handles the forensic costs to assess whether decryption is possible, the expenses to restore systems from backups, and the business interruption losses while your operations remain offline. Without this protection, you absorb these costs directly from cash reserves while your business sits idle.

Phishing and Social Engineering Attacks

Phishing and social engineering schemes represent the entry point for most breaches Minnesota companies face. Attackers send emails impersonating trusted vendors, customers, or internal executives, tricking employees into revealing passwords or clicking malicious links that install malware on your network. The Federal Communications Commission warns that phishing attacks have surged as remote work becomes standard, since employees working from home offices lack the same security infrastructure as office networks. A single compromised employee credential can give attackers access to your entire customer database, financial records, and proprietary information. Cyber liability policies that exclude social engineering attacks leave your business exposed to the most common attack vector you’ll face, so verifying your coverage explicitly includes phishing, spear phishing, and email-based fraud becomes non-negotiable when you evaluate policies.

Third-Party Vulnerabilities and Supply Chain Risks

Third-party vulnerabilities and supply chain risks expose your business to breaches you cannot control directly. Your software vendors, payment processors, cloud storage providers, and outsourced IT contractors all hold access to your systems and data. If any of these third parties suffer a breach, your customer information may be compromised even though you maintained strong internal security. Confirm whether your cyber liability policy covers liability arising from third-party breaches and whether it requires your vendors to maintain their own cyber insurance. The policy should also address whether you receive protection when a vendor’s security failure exposes your data (these incidents occur regularly across Minnesota industries and create legal exposure you didn’t anticipate).

Final Thoughts

Cyber liability coverage Minnesota businesses need protects against financial disasters that general policies ignore. The threats are real, the costs are substantial, and Minnesota’s compliance requirements demand immediate action when breaches occur. Your business faces ransomware attacks that halt operations, phishing schemes that compromise employee credentials, and third-party vulnerabilities beyond your direct control. A single incident can cost millions in forensic investigation, legal defense, notification expenses, and business interruption losses.

The coverage gaps in your current protection likely exceed what you realize. General liability policies leave cyber losses completely unprotected, while policies that exclude social engineering attacks expose you to the most common breach entry point. Coverage that doesn’t address third-party vendor risks leaves your business liable for breaches you cannot prevent directly, and stand-alone cyber policies designed specifically for digital threats provide substantially more comprehensive protection than cyber coverage added as an extension to existing policies. Compare deductibles across carriers, verify whether your policy covers both first-party losses and third-party liability, and confirm the specific attack types included (employee negligence and social engineering incidents matter significantly).

We at Maverick Risk Partners help Minnesota companies evaluate their cyber liability coverage and identify the gaps that create real financial exposure. Our carrier-neutral approach means we compare policies based on your actual operational risks rather than pushing a single carrier’s product. Contact us today to discuss a cyber liability coverage plan tailored to your Minnesota business.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional in our office for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.