Cyber Liability Policy Minnesota: Choosing the Right Policy for Your Firm

Minnesota businesses face mounting cyber threats that can cripple operations and drain resources. A cyber liability policy for a Minnesota business is no longer optional-it’s a business necessity.

We at Maverick Risk Partners help companies understand what coverage endorsements can protect them. This guide walks you through selecting the right policy for your specific needs.

Why Your Minnesota Firm Faces Real Cyber Threats

Small Businesses Are Prime Targets

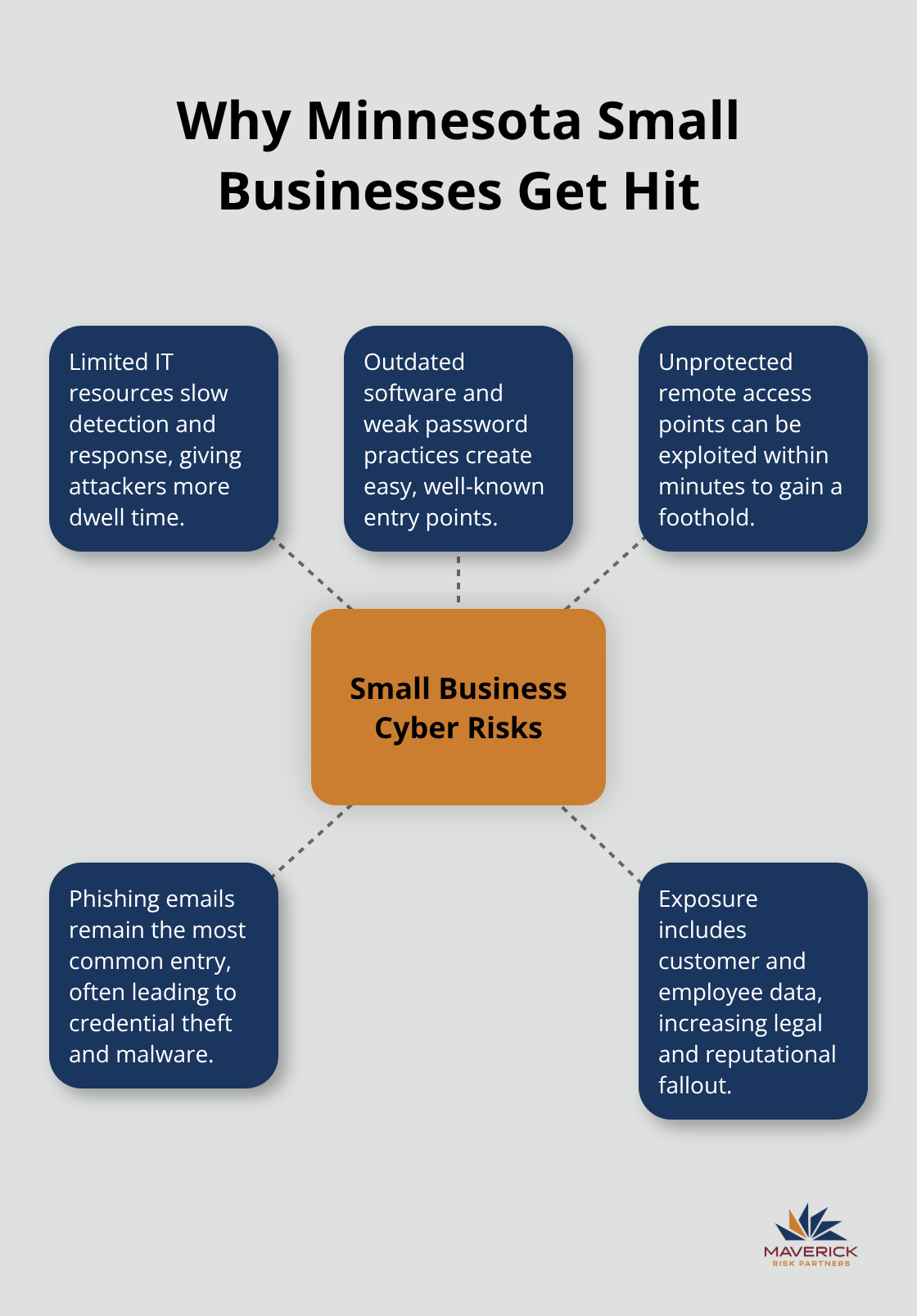

Small and mid-sized firms across Minnesota have become primary targets for cybercriminals, and the numbers prove it. Attackers deliberately target smaller operations because they know these firms handle sensitive customer and employee data while operating with limited IT resources.

Many Minnesota businesses still rely on outdated software, weak password practices, and unprotected remote access points-vulnerabilities that attackers exploit in minutes. Phishing remains the most common entry point, with a single employee clicking a fraudulent link impersonating a vendor, bank, or internal colleague leading to complete system compromise.

Remote Work Expands Your Attack Surface

Remote and hybrid work arrangements have expanded the attack surface dramatically. Without proper VPN encryption, multi-factor authentication, and endpoint protection, your workforce becomes a vulnerability rather than an asset. Attackers know that remote employees often work from unsecured networks and personal devices, making credential theft and malware installation far easier than attacks on office-based systems.

The Real Cost of Not Acting

The financial stakes are staggering. For Minnesota retailers, a ransomware attack means inoperable card payment systems and lost revenue during downtime. Law firms face locked access to client case files. Contractors cannot retrieve project documents. Online retailers cannot make sales.

Reputation and Compliance Damage

Beyond immediate operational losses, public breaches erode client trust, competitive standing and future business opportunity for years. Compliance violations add another layer-HIPAA violations, PCI DSS breaches, and Minnesota’s own data breach notification laws impose regulatory fines and investigation costs on top of incident response expenses. Minnesota’s regulatory environment under the Department of Commerce requires notification that a a cybersecurity event has occurred within a range of 24 hours to “without unreasonable delay” depending upon the breach details. This leaves minimal time to respond without proper planning and insurance support in place.

Understanding these threats sets the stage for evaluating what protection actually matters in a cyber liability policy.

What Coverage Actually Protects You After a Breach

A cyber liability policy covers far more than just the breach itself. The real protection lies in the costs that follow, and most Minnesota business owners underestimate what happens after attackers compromise their systems. The average cost to recover from a cyber incident reaches approximately $6.5 million per occurrence. Small businesses experienced a 46% cyberattack rate in 2025 with incidents occurring every 11 seconds. The average small business loss reached $120,000 per breach and 60% of companies attacked closed within 6 months.

Your policy needs to cover the forensic investigation that determines what was stolen, how attackers entered your systems, and whether they remain inside. Without forensic services, you operate blind during the most critical hours when containment decisions determine your final damage bill.

Notification and Legal Costs Add Up Fast

Data breach notification costs often surprise firms. You must notify affected customers, employees, and regulators within strict timelines. Cyber security firms often require a retainer to assist following a cyber attack. Without cyber insurance. or without the right cyber insurance policy, you would be faced with these expenses upfront. It would not be uncommon to have a forensic cyber firm require $5,000, $10,000 or $15,000 upfront to begin services.

Your policy should cover legal reviews of notification letters, notification services to send those letters at scale, credit monitoring and fraud resolution services for affected individuals, and call center operations to handle questions from worried customers and employees.

Third-Party Liability Protects Your Business Relationships

Network security liability protects you when your systems inadvertently expose customer data or when third parties claim you failed to protect information you stored on their behalf. This coverage matters especially for service firms handling sensitive client information such as law firms with case files, medical offices with patient records, and financial advisors managing account details. All of these types of professional service firms face third-party liability if data leaves your network.

Business Interruption Separates Survivors From Failures

Business interruption coverage reimburses lost income while your systems remain offline and restoration occurs. A single day of downtime for a retailer processing payments through compromised systems translates to thousands in lost transactions. Public relations and crisis management costs help you communicate with customers and media after a breach becomes public, protecting your reputation in tight business communities, online and in social media where word spreads fast.

Data Recovery and Identity Protection Complete Your Defense

The policy should cover data restoration expenses. The actual costs to recover, rebuild, and validate your data after malicious actors corrupt or delete it. Too many policies lack this coverage, leaving firms to absorb expensive data recovery services independently. Identity recovery protection extends to owners, employees, and affected customers, helping them restore credit histories and financial records after identity theft. Cyber extortion coverage reimburses ransom payments and related costs to the extent allowed by law if attackers encrypt your systems and demand payment. Making payments to cyber criminals can cause you legal issues without the proper support and compliance of an insurance provider.

Strong cyber insurance now requires you to maintain basic controls (multi-factor authentication, endpoint protection, regular backups, and access management) to qualify for coverage and avoid premium increases. Lacking these fundamentals can push you toward denial of coverage entirely when you need it most. The specific controls your carrier demands and the limits they offer vary significantly across policies, which means comparing what different insurers actually cover becomes your next critical step. Some leading cyber insurance carriers now offer you some of these cyber protection tools in addition to your cyber insurance policy, making it easier to be in compliance and know that you are protected.

Selecting a Policy That Matches Your Actual Risk

Identify Your Data and Regulatory Obligations

Start by identifying what data your firm actually handles and which regulations apply to your operations. A Minnesota medical office storing patient records under HIPAA faces fundamentally different cyber risks than a construction firm managing project schedules. Pull together an honest inventory of sensitive information you hold-customer payment data, employee Social Security numbers, health information, financial records-and determine which regulatory frameworks govern that data. PCI DSS applies if you process credit cards. HIPAA applies if you handle protected health information. GDPR applies if you serve European clients. Minnesota’s data breach notification law applies to all Minnesota firms.

Businesses operating in other states or who have clients in other states are subject to the data breach notification laws of each of those states. A retailer that sells online across all 50 states would need to comply with each of the 50 states’ compliance, regulatory and notification laws.

Starting with an assessment of the data you have access is the foundation that prevents you from purchasing coverage you don’t need while avoiding dangerous gaps in protection you do need. Many Minnesota firms skip this step and purchase generic policies that leave critical exposures uninsured.

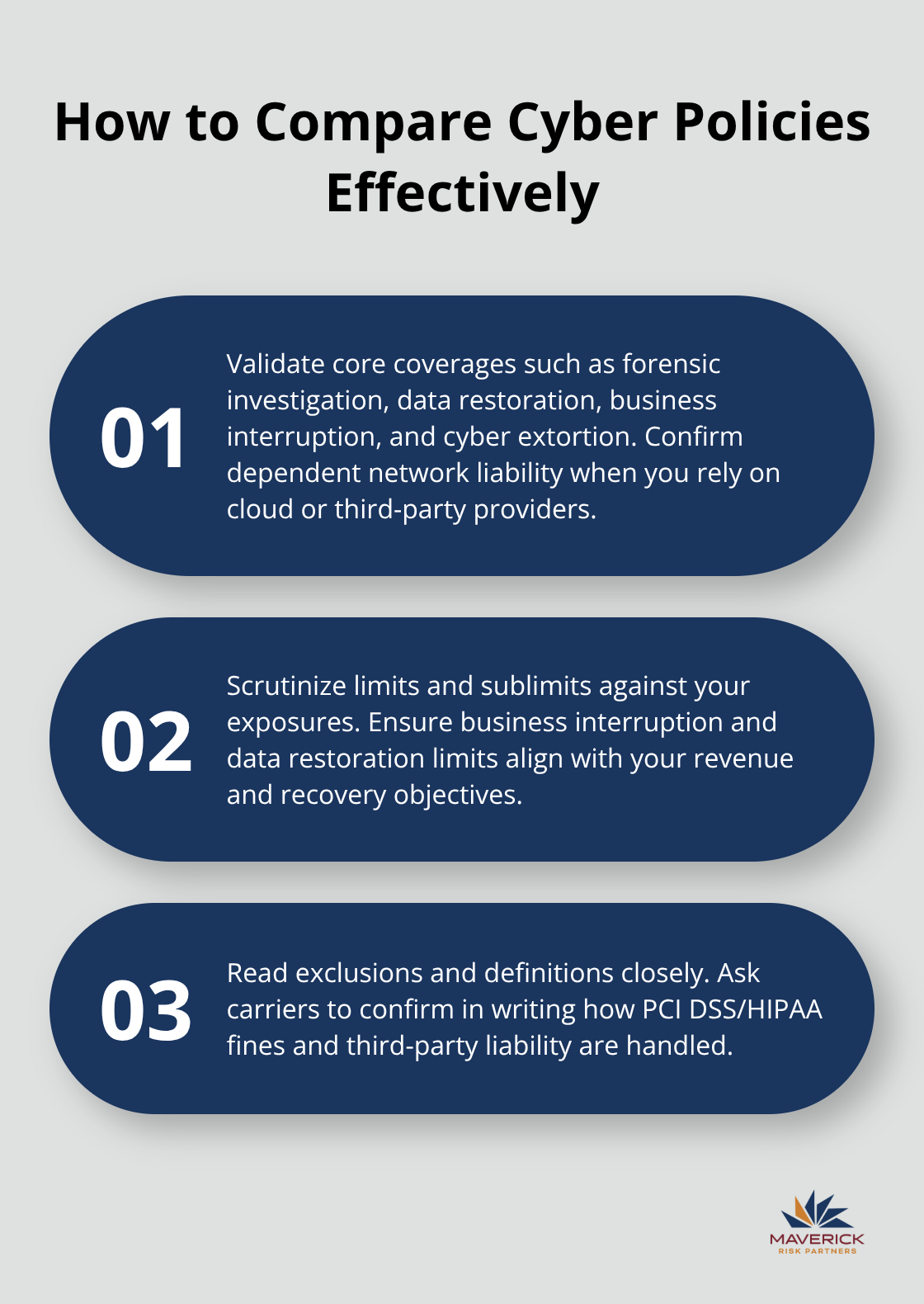

Compare Limits, Deductibles, and Actual Coverage

Compare specific policy limits and deductibles across carriers, because the differences matter far more than most business owners realize. Two policies might both advertise cyber liability coverage, but one includes data restoration costs while the other excludes them entirely. One carrier might cover business interruption losses up to $500,000 while another caps it at $100,000. One policy might include coverage for social engineering, and one may exclude it. One might include a crisis incident phone line for insurers to call they suspect an incident while another may expect you to secure your own forensics and request reimbursement after the fact.

When it comes to cyber extortion costs, some policies will pay those expenses on your behalf, while other policies require you to pay it yourself, and they will reimburse you. Cyber policies that have the reimbursement language can make it very difficult and expensive to settle a cybersecurity extortion event if you don’t have the right crypto funds to pay.

Make sure you understand whether a policy covers forensic investigation, network hardware restoration, cyber extortion, dependent network liability (covering losses from your cloud provider’s breach), and regulatory fines under PCI DSS or HIPAA. A Minnesota law firm should verify that third-party coverage extends to claims from clients whose information you stored. A retailer processing payments needs explicit business interruption coverage with clear definitions of what counts as covered downtime.

Evaluate Incident Response Support Beyond Claims Processing

Evaluate whether a carrier provides risk assessment services, incident response coaching, and claims support beyond simple reimbursement. When ransomware strikes or a data breach occurs, the difference between working with a carrier that offers immediate forensic support and one that simply processes claims months later determines whether your firm survives the incident or collapses under the pressure. Some carriers provide access to vetted forensic firms, legal counsel, and crisis management professionals as part of your policy. Others require you to find and hire these services yourself, then submit receipts for reimbursement. The second approach leaves you scrambling during the worst hours of your business life, making critical decisions without expert guidance while your systems remain compromised. At Maverick Risk Partners, we help Minnesota firms evaluate these differences and select carriers that provide the support your business actually needs when incidents occur.

Final Thoughts

Selecting the right cyber liability policy Minnesota requires matching coverage to your actual data, regulatory obligations, and operational vulnerabilities. We strongly recommend that you consider a dedicated cyber liability policy instead of a simple endorsement from a business owner’s insurance package. Verify that coverage extends to your specific risks-whether that means dependent network liability for cloud providers, PCI DSS fines for retailers, or HIPAA regulatory costs for medical practices.

Understand what incident response support each carrier will provide beyond claims processing, because the difference between immediate forensic guidance and delayed reimbursement determines whether your firm survives a breach intact. An agent tied to a single carrier has financial incentive to sell you that carrier’s policy regardless of whether it matches your needs. Carrier-neutral agents evaluate multiple insurers and selects the policy that protects your business the best.

We at Maverick Risk Partners help firms understand coverage gaps, negotiate better terms, and access carriers that provide incident response support when you need it most. Your cyber liability policy should reflect your specific risk profile, not a generic template that leaves dangerous exposures uninsured. Contact us to discuss your firm’s cyber protection needs and find the coverage that keeps your business running when attackers strike.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional in our office for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.