Lessor Risk Insurance Policy: What Landlords Need to Know

Owning rental properties comes with real financial exposure. Tenant damage, liability claims, and lost rental income can quickly drain your profits if you’re not properly protected.

Insurance carriers build lessor risk insurance policies specifically for landlords. They typically write these policies as commercial package policies combining building property coverage with commercial general liability for the premises. At Maverick Risk Partners, we help property owners understand exactly what protection they need and why it matters.

What Lessor Risk Insurance Actually Covers

Lessor risk insurance is a property and liability protection policy written specifically for landlords who lease commercial or residential space to tenants. Unlike standalone property policies that only protects the building structure, a lessor risk policy combines building with premises liability protection.

It responds to liability claims arising out of your ownership, maintenance, or control of the property, as well as property damage to the structure and permanent fixtures. Liability claims can come from your tenants, their employees, customers of your tenants and other service providers on your property. Your actual cost depends on your property type, tenant mix, location, and loss history.

This policy covers bodily injury or property damage lawsuits arising from conditions on premises you own or control, including claims brought by tenants, their employees, customers, vendors, delivery drivers, or other visitors. It also includes your legal defense costs if you face a covered lawsuit.

On the property side, it protects against common damage scenarios such as fire, smoke, wind, hail, water damage from burst pipes or sewer backups, theft, vandalism, and vehicle impact. If a covered loss makes a space unusable, the policy can include rental value or business income coverage depending on policy language.

How a Lessor Risk Policy Differs from Standard Business Coverage

Standard commercial property insurance protects the building structure itself. However, it does not include liability coverage. In contrast, a lessor risk policy combines property protection with commercial general liability for premises exposures. Therefore, a property-only policy will not cover bodily injury lawsuits or legal defense costs for tenant or 3rd party claims. Many landlords mistakenly assume their property policy handles liability, but it does not.

The key difference between a lessor risk and a standard business policy lies in scope. A lessor risk policy insures premises liability tied to property ownership. It also addresses liability arising from a tenant’s business operations and your management of a property.

Your policy protects you for injuries or damage connected to areas you own or control, such as parking lots, hallways, stairwells, sidewalks, and structural components. Meanwhile, the tenant’s general liability policy, often called a Business-Owners Policy or BOP, responds to claims arising out of their specific business activities inside their leased premises.

Building Your Protection Strategy

Many landlords require tenants to carry general liability with the landlord named as an additional insured. This requirement adds another layer of protection. As a result, it strengthens your defense against claims that might otherwise fall on your shoulders.

Premium factors vary significantly by location, construction materials, occupancy rates, and safety features like smoke detectors or burglar alarms. Consequently, properties in densely populated or higher-crime areas can cost more to insure. By understanding these cost drivers, you can better identify your property coverage and which protections matter most for your situation.

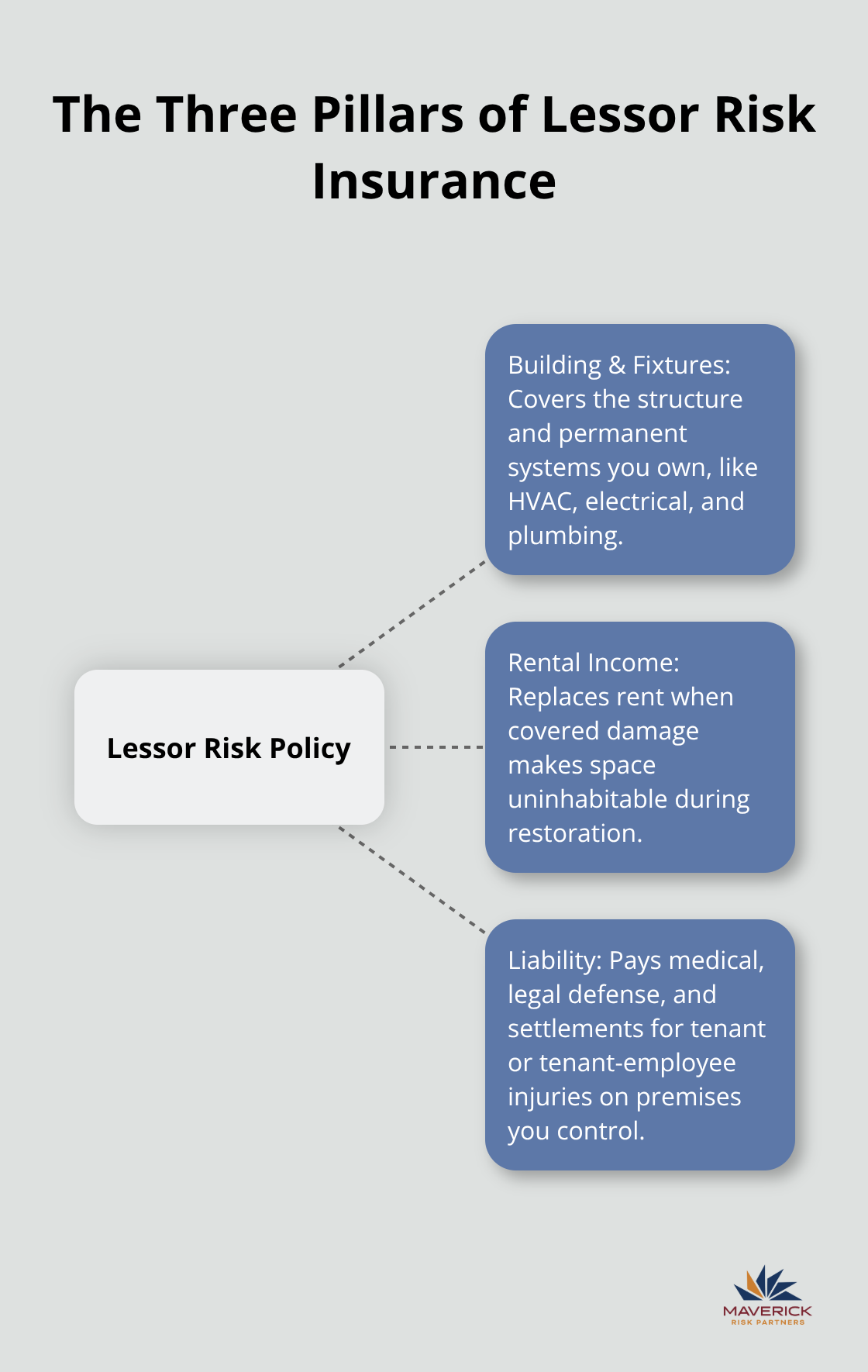

What Your Lessor Risk Policy Actually Protects

Lessor risk insurance covers three distinct areas that matter most to your bottom line. First, it protects the physical structure and permanent fixtures you own. Second, it protects your rental income when a property becomes uninhabitable. Third, it protects your liability exposure arising out of ownership, maintenance, or control of the premises when someone gets injured on premises you control.

The Hartford reports that lessor risk policies typically cost around $1,972 per year on average. Your actual premium depends on the value or cost of your building, the deductible you choose, which coverages you select and how aggressively you want to protect each exposure.

Most landlords mistakenly think one coverage level fits all scenarios. In reality, your property type, tenant mix, and local risk profile should dictate exactly what you purchase.

Protecting Your Building and What’s Attached to It

Your building structure and permanent fixtures like HVAC systems, electrical wiring, plumbing, and built-in appliances represent your largest asset in a rental property. A lessor risk policy covers damage to these items from fire, smoke, wind, hail, water damage from burst pipes or sewer backups, theft, vandalism, and vehicle accidents on the property.

For example, if a tenant’s negligence causes a pipe to burst and damages the walls, flooring, and electrical systems, your lessor risk policy covers those repairs. This coverage applies to the structure and landlord owned improvements. It does not apply to the tenant’s personal property, inventory, or business equipment inside the leased space. Tenants must insure their own contents and operational exposures under their separate policies.

Construction type plays a significant role in premium development. Fire resistant construction typically costs less to insure than older wood frame buildings. Location also impacts pricing, especially in densely populated areas or regions with higher crime or catastrophe exposure.

Additionally, safety features such as monitored alarms, sprinkler systems, and properly maintained smoke detectors can reduce both risk and premium. Therefore, proactive property management remains an important part of your overall protection strategy.

Income Protection When Tenants Can’t Occupy Space

Loss of rental income coverage, often written as rental value or business income coverage, compensates you for lost rent during the restoration period after a covered cause of loss damages the property.

For instance, if a fire makes a unit uninhabitable for three months while repairs are completed, this coverage replaces the lost rental income so your cash flow remains stable. Because rental income often represents the primary return on investment, this protection is critical.

The duration of loss of rental income coverage varies by policy. Therefore, you should confirm exactly how long your insurer will compensate you after a covered loss occurs. Some policies cover only the time needed for physical repairs. Others extend coverage through a defined restoration period.

The difference can mean thousands of dollars in protection, especially for multi-unit properties where vacancy costs multiply quickly. Without this coverage, you absorb the full cost of lost income while also paying for repairs. As a result, your investment strategy can face significant financial strain.

Liability Claims From Tenant-Related Injuries

Liability protection shields you from expenses and legal costs when someone is injured on premises you own or control. This includes tenants, their employees, customers, delivery drivers, vendors, or members of the general public.

If a person slips in a common hallway due to inadequate maintenance or poor lighting, that exposure typically falls under your premises liability coverage as the landlord or building owner. A properly structured lessor risk policy includes commercial general liability that responds to covered claims. This coverage includes legal defense costs, settlements, or judgments up to your policy limits.

Higher occupancy properties and buildings with higher-risk tenants such as restaurants or gyms, or properties with significant public foot traffic, may face elevated liability premiums. Increased activity raises the likelihood of injury claims.

Tenant type also matters from an underwriting perspective. Mixed-use properties receive ratings based on the riskiest tenant category present. A building with one restaurant tenant among five office tenants may see premium increases driven by that single high-risk occupant.

Your lease should require tenants to carry their own general liability insurance and name you as an additional insured on a primary and non-contributory basis. Your lease should also include these indemnification requests. Therefore, review your tenant lease for proper language. This added layer of protection helps ensure that claims arising out of the tenant’s operations go to their policy first.

Understanding these three protection areas helps you identify which exposures pose the greatest financial risk to your specific property. Next, we examine the coverage gaps that catch most landlords off guard and explain why standard policies leave you vulnerable.

Where Lessor Risk Insurance Falls Short

Most landlords discover coverage gaps only after a loss occurs. By then, the financial damage has already occurred.

Although lessor risk insurance protects you from many exposures, it does not cover the tenant’s business property, the tenant’s personal belongings, or certain excluded causes of loss outlined in the policy.

If a tenant intentionally sets a fire or deliberately damages the unit, coverage will depend on the specific policy form and circumstances of the loss. Property policies generally cover accidental direct physical loss. However, intentional or criminal acts may trigger exclusions or require additional investigation. Because coverage determinations depend on specific facts, insurers evaluate the cause of loss carefully before approving or denying a claim.

Tenant-Caused Damage and Property Protection Gaps

Tenant caused damage resulting from negligence typically triggers coverage for the building structure and landlord owned improvements, subject to policy terms and deductibles. However, coverage does not extend to the tenant’s equipment, inventory, or furnishings inside their leased space. Tenants must carry their own property insurance to protect those items. Unfortunately, many fail to maintain adequate coverage.

If your tenant has completed “tenant betterments and improvements”, your lease should require them to insure that financial investment. If your lease does not include that requirement, then you need to increase the building insured value to account for that financial investment from the landlord for the build-out. In addition, review coverage limits to make sure they remain adequate and accurate.

Your lease agreement should explicitly require tenants to maintain appropriate property and liability insurance. If your tenant does not carry a proper business-owner’s policy and there is a loss at your building, they may not continue purchase the necessary business personal property they need to run their business. They may not have funds to pay rent and return to the space after the loss.

Unlike liability policies, insurers do not typically name landlords as additional insureds on a tenant’s property policy. However, you can require proof of coverage and monitor compliance to reduce disputes after a loss.

Natural Disasters and Weather Exclusions

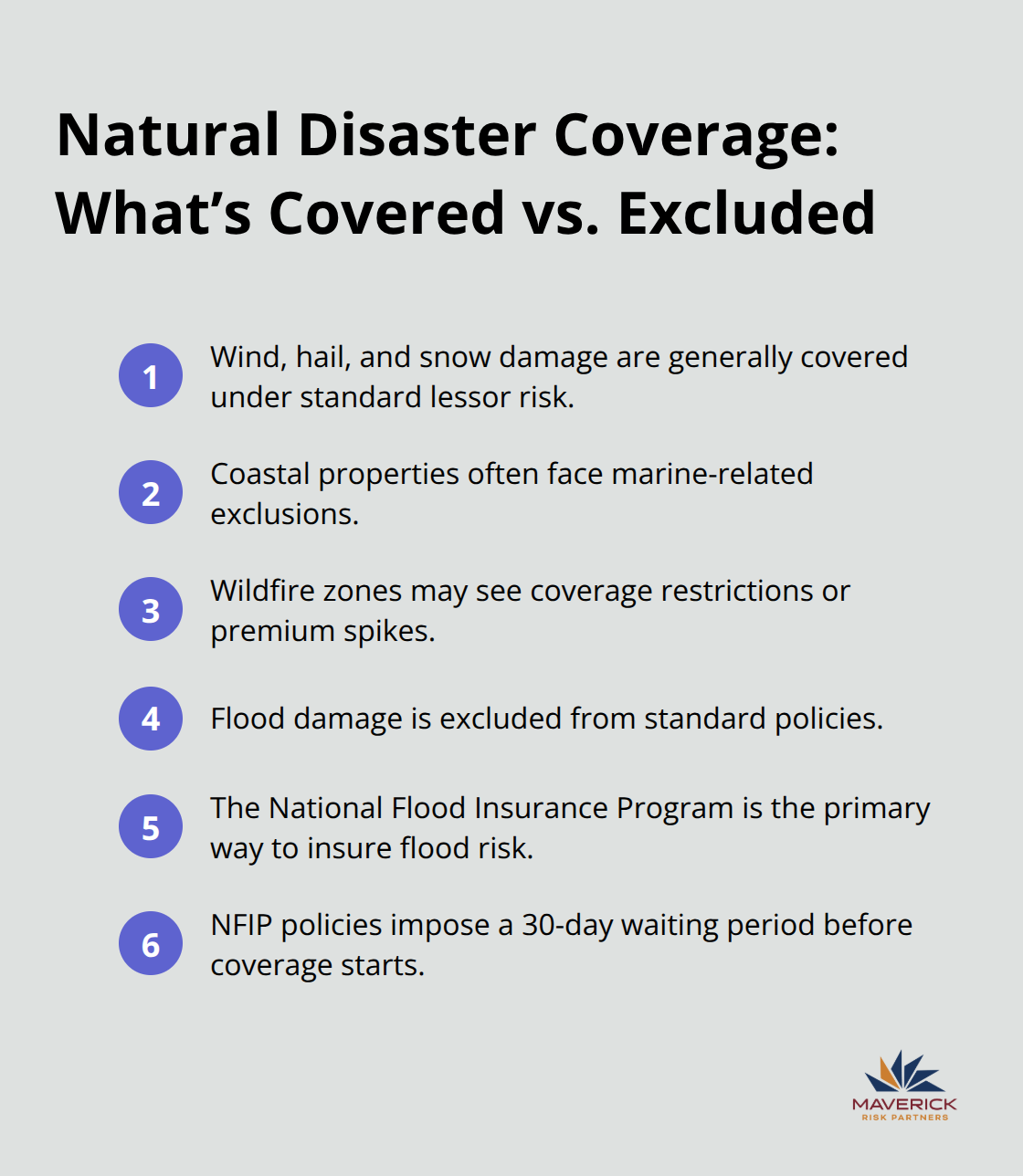

Natural disasters and weather events create frequent misunderstandings. Lessor risk policies generally cover standard weather related damage such as wind, hail, and certain storm events, subject to policy conditions and deductibles. However, standard commercial property forms exclude flood damage regardless of location. Therefore, you must secure separate flood insurance through the National Flood Insurance Program or private flood market to insure that exposure.

Some policy forms exclude damage or claims from the weight of ice or snow, collapse, water damage, theft or vandalism, civil commotion or riot, or equipment breakdown. However, you can include these risks by selecting the right coverage form or adding endorsements.

Coastal properties may also face windstorm deductibles or separate wind coverage requirements. Similarly, wildfire exposed areas may experience underwriting restrictions or premium increases depending on carrier appetite. Because coverage availability and terms vary significantly by location and insurer, you should review catastrophe exposures carefully.

Properties in designated high risk flood zones generally must carry flood insurance if lenders finance them with federally backed mortgages. Even then, some landlords carry only the minimum limits necessary to satisfy lending requirements. As a result, those limits may not fully protect their investment.

In wildfire prone areas, particularly in parts of the western United States, some carriers have tightened underwriting guidelines, limited capacity, or increased premiums and deductibles for properties with elevated catastrophe exposure. Because natural disaster risk varies significantly by geography, you should evaluate your specific location and exposures rather than assume a standard property policy will address every potential catastrophe risk.

Third-Party Liability and Lease Requirements

Liability claims involving injuries on the property can create confusion about which policy responds. A lessor risk policy typically includes commercial general liability coverage for bodily injury or property damage arising out of your ownership, maintenance, or control of the premises, including common areas.

If a delivery driver, contractor, customer, or other visitor suffers an injury due to a condition in an area you control, your policy may respond. However, if the injury arises out of the tenant’s business operations or a hazard created within the tenant’s leased space, the tenant’s general liability policy should respond first.

Your lease should require the tenant to maintain general liability insurance with limits appropriate for their operations. It should also require them to name you as an additional insured on a primary and non-contributory basis so their policy pays first. Proper risk transfer directs claims to the appropriate policy and reduces disputes between carriers. Without this lease requirement, you could become the secondary payer and absorb costs the tenant’s insurer should cover. In addition, the claim can negatively impact availability of coverage and your rates.

Standard lessor risk forms do not cover eviction related legal expenses. However, some minor tenant-related coverages can provide extra protections. You usually find those in preferred policy forms or enhanced endorsements.

Final Thoughts

Your lessor risk insurance decisions should align coverage with your specific property exposures rather than rely on generic recommendations.

First, document your current coverage. Next, identify which risks present the greatest financial threat to your rental income and assets. Then, review your lease agreements to confirm tenants carry appropriate general liability coverage with you named as an additional insured.

Natural disaster exposures require particular attention based on location. If you own property in a flood prone area, you need separate flood insurance through the National Flood Insurance Program or a private flood market, since standard commercial property policies do not cover flood damage. Coastal and wildfire exposed properties may also require additional review due to underwriting limitations, deductibles, or carrier restrictions.

We at Maverick Risk Partners provide consultative, carrier-neutral advice that matches your coverage to your actual exposures rather than recommending unnecessary policies or removing important coverages just to create a low attractive cost. Our team handles the complexity of lessor risk insurance so you can focus on growing your real estate portfolio with clarity and confidence.

Contact us today to review your current protection strategy and identify potential gaps before they become costly problems that could derail your investment strategy.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional in our office for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.